Contrasting Cruise, Waymo, and Tesla's Go To Market Strategy for Autonomy

There's many paths, but hopefully only one destination

Cruise began giving driverless rides to the public on 2/1/22. Woo! As William Gibson said, the future is already here - it’s just not evenly distributed.

This is a major milestone for Cruise and transportation overall. However, Cruise is not the only one giving driverless rides in the USA and they are certainly not the only one seeking to be the leading player in autonomy.

Waymo has been giving fully driverless rides to the public since October 2020 in the Chandler, Arizona area (East Phoenix) and recently announced service coming to San Francisco

Tesla has been having “Full Self Driving” (FSD) available to drivers since October 2020. It is hardly fully self driving considering drivers need to keep their hands on the wheel. However, there are over 60,000 drivers in the beta program and its constantly being updated.

Zoox is doing test drives on semi-public tracks

Aurora is testing in Texas, California, and Pittsburgh

Nuro is already doing deliveries

Motional is testing in Las Vegas and elswhere

Argo.AI is testing in Miami, Austin, Detroit, CA and more

And there’s a host of other companies testing solutions including Woven Planet (acquirer of Lyft’s Level 5 self driving division)

For a breakdown of all the companies operating in CA, you can see my last post here.

Certainly though, Cruise is operating in the densest US city of anyone.

SF population per sq mi - 6266

Chandler population per sq mi - 4200

Let’s dig into the different go-to-market approaches by Cruise, Waymo, and Tesla.

I’m digging into these because I have the most context on their publicly available services, not to say that they are the only contenders. I will recap their current scale, how they are limiting risk as they go to market, and what advantages they may have looking ahead. First though, let’s recap why autonomy is hard.

Why Autonomy is Exciting, but also very hard

Autonomy will be a major technical feat and commercial prize for any automaker. For society, it will represent a significant reduction in anxiety, tens of thousands of lives saved every year, and a way to make rideshare’s convenience more accessible in both price and utility. But there’s still a significant, decade-long way to go.

Autonomous transportation providers need to have reliable, swift performance across time of day, geography, and environment. The vehicles need to drive themselves safely and protect their riders as well as cargo. But they also need to adapt to the road environment around them which could include pedestrians, stop and go delivery drivers, and even those who are driving drunk. This needs to be across various weather patterns, cultural driving norms (such as the odd Michigan Left), and road designs. And they need to do this while obeying current laws while also shaping future policy in order to be suited for a new normal. It’s hard.

The autonomous providers they need to keep society’s trust so that the environment remains favorable and consumers are even willing to give it a try (Uber’s fatal AZ collision was a setback). A March 2021 Morning Brew-Harris Poll survey found that just 48% of US adults would be somewhat comfortable in the passenger seat of an AV. These companies will certainly be insolvent if they don’t have customers.

This is hard.

Current Scale of each provider

Cruise

Cruise is now giving fully driverless rides to the public in San Francisco. Soon they even plan to charge for them. A month ago they submitted a petition to NHTSA for a formal review of their self-driving shuttle design, the Origin.

Per the CA DMV’s disengagement report, Cruise had 137 vehicles operating in California at the end of 2021. I expect that number to go up this year as people try out Cruise’s rideshare service. They have other trials planned including in Scottsdale and in Dubai.

They are an SF-based company, majority owned by General Motors, and have been testing on the roads there for years. They have raised $13B, nearly enough to buy Lyft at today’s stock price.

Waymo

Waymo is giving fully driverless rides in a 50 square mile area in East Phoenix, including Chandler, AZ. They, with disowned alum Anthony Levandowski, are the pioneers in autonomy and started efforts within the Google Umbrella in 2009.

Per the CA DMV’s disengagement report, Waymo had up to 700 vehicles operating in the state by the end of 2021. Further, they had the highest amount of autonomous miles driven in CA at 2.1M. They just announced that Waymo Driver will no longer have a specialist behind the wheel in San Francisco.

Tesla

Tesla has sold over 2,370,000 connected vehicles since 2013. Over 2,200,000 deliveries with its Autopilot Hardware 2/3. 60,000 drivers are enrolled in its Full Self Driving (FSD) beta program across the world. That’s up from 1,000 in October 2021.

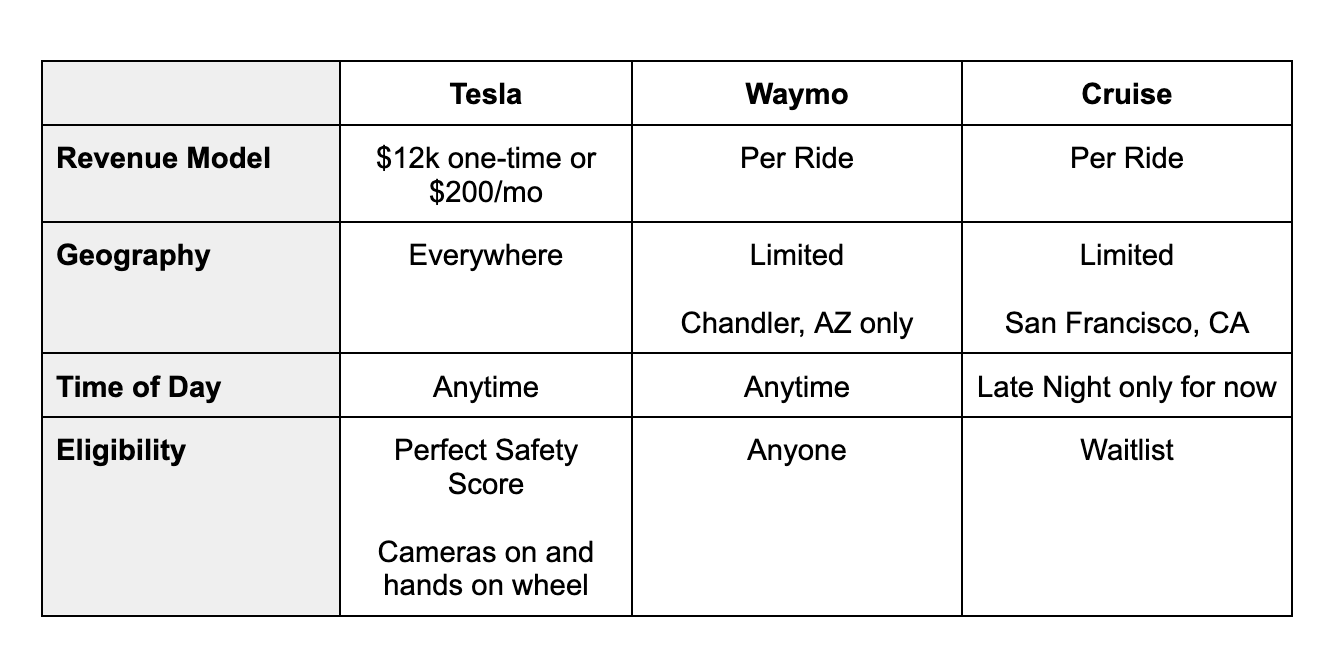

Limiting Risk

Each company wants to successfully bring their technology to market, but they need the right conditions. It’s about finding the wedge market and limiting the variables that could cause autonomy to fail. Once they have that wedge, they can iterate and expand. Each is taking a different approach.

Tesla

Tesla’s FSD Beta is available to any driver whose vehicle has Autopilot 2/3 hardware stack and who has paid for the feature ($12k one-time or $200/mo). The service can be used anywhere and at any time, with different performance in different conditions.

To use FSD though, Tesla has some safety hurdles that drivers need to pass:

Drivers need to have a perfect safety score

Drivers need to have their hands on the wheel

Drivers need to have internal and external cameras turned on

Waymo

Waymo is operating for the public only in a 50 sq mi region near Chandler, AZ. This constrains the risks because the weather is relatively uniform and the city design is fairly modern.

Anyone in Chandler can use the service, though it doesn’t seem wildly popular yet.

Cruise

Cruise is operating for the public only in San Francisco (49 sq mi) and right now seemingly only at night. By operating only at night, there’s less visual variation and less vehicles on the road. Plus it might be that the mix of vehicles on the road at that time involves more rideshare vehicles.

San Francisco’s weather is also fairly consistent.

One additional advantage of starting in San Francisco is the density of early adopters. After all, this is where Uber and Lyft started.

One observation comparing these is that Tesla seems to be selling a capability whereas Waymo and Cruise are selling a service. The capability is available wherever the car can go, but that doesn’t mean that it will always work as well. The same way that 2 Wheel Driving cars don’t work as well in snow. On the other hand, if Cruise and Waymo are available, they are selling you a perfectly smooth, safe ride.

Driving to the future

Looking ahead, each company’s approach has its own advantages and disadvantages.

Tesla clearly has the revenue advantage. They don’t actually have demand risk considering they already have at least 60,000 paying customers. That high-margin software revenue helps make Tesla the most profitable automaker.

Tesla also may have the data advantage. It has many more vehicles in many more places attempting to drive autonomously. That feedback loop can be powerful, as long as the data is being contextualized as an input. Using data from Norway to inform expectations of Texan drivers might not always make sense. Waymo and Cruise’s approach, in addition to having more expensive hardware to gather better quality data, allows for more specific solutions.

On a sequencing and time to market basis, it seems Waymo had an advantage but that has most likely been squandered. Cruise is now live. And Cruise is live in places where they will most likely build a density.

That’s not to say Waymo can’t catch up - Google employees alone make up tens of thousands of people in the Bay Area. Further, Google Maps has over a Billion monthly active users that Waymo could tap into. Musk’s twitter audience is at best ~7% the size of that. GM/Cruise don’t even come close in terms of # of connected customers.

From a regulatory lens, Waymo and Cruise seem to have the advantage. Cruise and Waymo have deliberately worked with local authorities and Cruise has even applied to NHTSA to certify their vehicle. On the other hand, Tesla is technically selling a product that isn’t fully working. It’s not fully self driving. Regulators thus far haven’t taken adverse action, but there has been plenty of investigation and consideration. Tesla’s software could be forcibly recalled with a bad enough incident attributable to FSD. Interestingly, that would only be an over-the-air update.

“Having machines run over people, that would be unpalatable.” - John Casesa, who steered the Argo AI investment as Ford’s head of global strategy

The hardest to evaluate is consumer trust. Tesla may have some advantages because of scale. There are so many more of them on the road that a large % of the population has possibly already sat in a Tesla vehicle operating with Autopilot. That’s important because that same Morning Brew survey found the best predictor of consumer trust was if someone had previously taken an autonomous ride.

I do like that Cruise and Waymo have designed their vehicles to look cute and maybe even soft. Cruise’s vehicles are even named after tasty food like Baos, Burritos, and Tostadas! It helps make the vehicles more approachable and reduces the fear of a murderous autonomous robot.

One additional factor into trust is that Tesla has much more of an aspirational brand than either Waymo or Cruise right now. If someone is going to take a risk, until they see a Waymo or Cruise in action, Tesla has more gut pull and excitement.

It’s early though. The most trusted company is clearly going to be the one whose service works reliably.